COVID-19 Survival Blog #4 - Emergency Funding

COVID-19 Survival Blog #4 - Emergency Funding

Emergency Funding: How Much, and Where

Based on comments from readers of the last post, it seems like people don't mind when I go full nerd on calculations and numbers, so let's do one more post like that, and next time I'll talk about something we did that was a little more fun. Sound good?

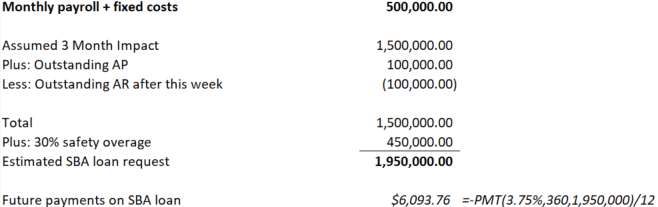

Picking up where we left off from last post, we had our figure for the estimated amount of emergency funding that we needed. Since it's probably helpful to see some numbers in these calculations, here's how the bottom of our spreadsheet looked, but with fake numbers (since we're not requesting nearly this much, thankfully):

This is considering the advertised SBA Emergency Loan terms, which are 3.75% interest rate over 30 years. If you've never used the PMT function in Excel, it's handy, and I showed how to do it next to the future monthly payments calculation (360 represents the number of months, and 1.95m is the loan request), but you could also use a payment calculator via a quick Google search.

If you know you'll need emergency funds, definitely apply at the SBA's website, here:

https://covid19relief.sba.gov/#/

We enjoyed it so much, we did it twice! The SBA has hilariously changed their application process three different times since this all started, for multiple reasons that you can read in the news. But the latest change came after the passing of the CARES Act, which provided for a $10,000 emergency advance, so getting that was the reason we applied the second time (still no 10 Gs yet as I write this, FYI). They told people to apply again and that it wouldn't hold up their original app, so for your peace of mind, no, we weren't trying to scam the system.

At the time of our first application, we didn't know whether the CARES Act would exist yet, much less what would be in it, so we took the expected future payments over the next 30 years (the fake $6,093.76 figure above) as a barometer for what impact we thought we could stomach to our monthly cash flow going forward as a result of the funds we would need to take out. It was particularly helpful in deciding what payroll we could maintain during the down time.

Once the CARES Act was signed and details were released, it didn't change the anticipated emergency funding that we need, but thanks to the Paycheck Protection Program (PPP) loan provision in the Act, we were now told that if we obtained some of our emergency funds through that program, a portion of it would be forgiven. So off we went to apply for this loan as well.

We've been asked this question a few times: Should I apply for both? YES. DEFINITELY. FOR AS MUCH AS YOU CAN REASONABLY SUPPORT.

First off, the PPP is limited in amount to 2.5x your average monthly payroll, usually based on your 2019 tax forms (we used our W-2 Summary, Box 1 and our 941 payroll tax filings, Box 2, to support it further), but I'll edit this in the future if the bank wants to use a different document, or a different method of calculation). And secondly, both of these loans have such favorable terms, that with the climate of total uncertainty right now, our opinion has been that it would be better to overshoot our funding request (again, within reason) and in the worst case, pay whatever is not needed back when we feel like we're completely out of the woods. In our case, this would be after another slow season (late fall, all of winter, and early spring).

I thought about going through our interpretation of what amounts will be forgiven and the general terms of the PPP loan, but honestly we're still reading the material and trying to estimate that ourselves. Whatever it ends up being though, any forgiveness is better than the original $0 of forgiveness we were expecting on the standard disaster loan directly through the SBA.

Also, the clearest interpretation (read: clearer, but still with LOTS of ambiguity) we've seen so far comes right from Treasury's fact sheet for borrowers on their website:

https://home.treasury.gov/system/files/136/PPP--Fact-Sheet.pdf

Ok, almost done with the full-scale nerdery. Last thing I will say is that if you haven't approached your bank about the PPP loan, DO IT NOW. They're probably still in shock because this is all happening very quickly for them, so be gentle. Still, come prepared. They may not have their own application yet, but bring them this standard one provided by the Treasury:

https://home.treasury.gov/system/files/136/Paycheck-Protection-Program-Application-3-30-2020-v3.pdf

Come as prepared as you can. Fill out the application completely. Support your figures with tax documents and Excel calculations so that your banker has to do as little work as possible. They'll appreciate it, and you'll end up higher up in the queue for your efforts (I assume). The lines are already forming in bankers' inboxes, so get on it, and be thorough.

Alrightalrightalright. Even I am sick of all the money talk now, but we felt like we had to put all of this out there as early as possible since this landscape is changing so quickly.

Next up - a post about something fun we did, as promised!